![]()

2025 The Most Effective 8011 with 330 Questions Answers

Try Free and Start Using Realistic Verified 8011 Dumps Instantly.

PRMIA 8011 (Credit and Counterparty Manager (CCRM) Certificate) Certification Exam is a globally recognized certification exam that tests the knowledge and skills necessary for credit risk management in the financial industry. 8011 exam is designed for professionals working in the areas of credit risk management, debt and capital markets, finance, and banking. The PRMIA 8011 CCRM Certificate is an accreditation that demonstrates an individual's ability to minimize the credit risk of a financial institution while maximizing the return on investment.

PRMIA 8011 Credit and Counterparty Manager (CCRM) Certificate Exam is a highly respected certification that is valued by employers and recognized globally as a mark of excellence in the field of credit and counterparty risk management. 8011 exam is designed to test an individual's knowledge and understanding of the key principles and practices of credit risk management and counterparty credit risk management, and is open to professionals who meet the eligibility requirements. With its comprehensive syllabus, rigorous testing, and global recognition, the PRMIA 8011 CCRM certification is an essential credential for anyone looking to advance their career in risk management.

PRMIA 8011 CCRM exam is a rigorous, comprehensive, and challenging exam that requires a significant amount of preparation and study. It is designed for professionals who are looking to advance their careers in credit and counterparty risk management, and who want to demonstrate their knowledge and expertise in this important field. 8011 exam is open to anyone who meets the eligibility requirements, which include a minimum of two years of relevant work experience in credit risk management and a bachelor's degree or higher.

NEW QUESTION # 122

An error by a third party service provider results in a loss to a client that the bank has to make up. Such as loss would be categorized per Basel II operational risk categories as:

- A. Abnormal loss

- B. Outsourcing loss

- C. Execution delivery and process management

- D. Business disruption and process failure

Answer: C

Explanation:

Choice 'a' is the correct answer. Refer to the detailed loss event type classification under Basel II (see Annex 9 of the accord). You should know the exact names of all loss event types, and examples of each.

NEW QUESTION # 123

The diversification effect is responsible for:

- A. the super-additivity property of market risk VaR assessments

- B. total VaR numbers being greater than the sum of the individual VaRs for underlying portfolios

- C. VaR being applicable only to short term horizons

- D. the sub-additivity property of market risk VaR assessments

Answer: D

Explanation:

Any good risk measure has the property that it is sub-additive, which means the whole is less than the sum of the parts. In the case of VaR, sub-additivity arises due to the diversification effect, or said differently, due to the correlation between different assets being less than one. Therefore Choice 'd' is the correct answer.

Super-additivity is just the opposite of sub-additivity, ie, the whole is greater than the sum of the parts. Good risk measures do not have super-additivity. Therefore Choice 'b' is incorrect.

Choice 'c' states the same thing as Choice 'b' in different words, and is incorrect. Choice 'a' is non-sensical and incorrect.

NEW QUESTION # 124

Under the CreditPortfolio View approach to credit risk modeling, which of the following bestdescribes the conditional transition matrix:

- A. The conditional transition matrix is the unconditional transition matrix adjusted for probabilities of defaults

- B. The conditional transition matrix is the transition matrix adjusted for the distribution of the firms' asset returns

- C. The conditional transition matrix is the unconditional transition matrix adjusted for the state of the economy and other macro economic factors being modeled

- D. The conditional transition matrix is the transition matrix adjusted for the risk horizon being different from that of the transition matrix

Answer: C

Explanation:

Under the CreditPortfolio View approach, the credit rating transition matrix is adjusted for the state of the economy in a way as to increase the probability of defaults when the economy is not doing well, and vice versa. Therefore Choice 'a' is the correct answer. The other choices represent nonsensical options.

NEW QUESTION # 125

The systemic manifestation of the liquidity crisis during the current credit crisis took many forms. Which of the following is not one of those forms?

- A. Drying up of liquidity in the corporate bond markets

- B. Drying up of liquidity in the cash market for treasury bonds

- C. Stress and large withdrawals from the money markets

- D. Drying up of liquidity in the wholesale money markets

Answer: B

Explanation:

The stresses on liquidity that happened as part of the credit crisis beginning 2007-08 led to drying up of trading and liquidity crisis in the corporate bond markets, the auction rate securities markets, the wholesale (interbank lending) markets, the money markets, the markets for structured products, and even the otherwise liquid futures and forwards markets (as there was no liquidity available to fund the financing of futures). The one market that was not affected was the market for treasuries, in fact the flight to quality ensured that this market was very liquid (even though stressed from a pricing perspective as yields plummetted).

Therefore Choice 'a' is the correct answer.

NEW QUESTION # 126

For credit risk calculations, correlation between the asset values of two issuers is often proxied with:

- A. Credit migration matrices

- B. Default correlations

- C. Transition probabilities

- D. Equity correlations

Answer: D

Explanation:

Asset returns are relevant for credit risk models where a default is related to the value of the assets of the firm falling below the default threshold. When assessing credit risk for portfolios with multiple credit assets, it becomes necessary to know the asset correlations of the different firms. Since this data is rarely available, it is very common to approximate asset correlations using equity prices. Equity correlations are used as proxies for asset correlation, therefore Choice 'c' is the correct answer.

NEW QUESTION # 127

The accuracy of a VaR estimate based on a Monte carlo simulation of portfolio prices is affected by:

I). The shape of the distribution of portfolio values

II). The number simulations carried out

III). The confidence level selected for the VaR estimate

- A. II

- B. III

- C. II and III

- D. I, II and III

Answer: D

Explanation:

VaR calculations look at the lower part of the distribution of future portfolio values, for example, if the desired confidence level is 95%, the cut-off for the VaR calculation will be at the bottom 5%; similarly at 1% for a 99% confidence level. The number of observations that will end up in these bottom ranges will be few and sparse, and therefore their accuracy will generally be lower than, say, the average where observations are more likely to be concentratred. If the shape of the distribution of future portfolio values is not symmetrical and has a long tail to the left, then this problem gets further exacerbated as there may be even fewer and less reliable simulated numbers at the 5% or 1% quintiles. Thus the shape of the distribution will affect the accuracy of a VaR estimate. The distribution for a short option position, for example, will have a long tail to the left, and the VaR number will be quite significantly affected by a few simulations. On the other hand, for a long option position where the long tail is to the right, and we are interested in the left tail which is better defined and ends at zero we are more likely to get a better VaR estimate. Therefore Statement I is correct.

The number of simulations carried out directly affects the standard error, which is inversely proportional to the square root of the sample size (ie the number of simulations). THe accuracy of the VaR estimate can be increased by increasing the sample size (or reduced by reducing the sample size). Therefore Statement II is correct.

The confidence level selected for the VaR estimate also affects the accuracy of the estimate. Tointuitively understand this, consider this extreme example where the desired confidence level is 99.9% and there are

1000 observations. Therefore the VaR will be determined by the last value in the sample, and will therefore be quite fickle and dependent upon what chance produces as the lowest value in the simulation. But if for the same sample the confidence level desired were to be 90%, there would be 100 observations beyond the 90% cut-off and this would be a much more stable and accurate number. Therefore the confidence level selected for the VaR estimate is also a determinant of the accuracy of the VaR estimate derived from the simulation.

Statement III is correct.

Thus all statements are correct and Choice 'b' is the correct answer.

NEW QUESTION # 128

For a hypotherical UoM, the number of losses in two non-overlapping datasets is 24 and 32 respectively. The Pareto tail parameters for the two datasets calculated using the maximum likelihood estimation method are 2 and 3. What is an estimate of the tail parameter of the combined dataset?

- A. 0

- B. 2.57

- C. Cannot be determined

- D. 2.23

Answer: B

Explanation:

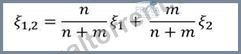

For a number of processes, including many in finance, while a distribution such as the normal distribution is a good approximation of the distribution near the modal value of the variable, the same normal distribution may not be a good estimate of the tails. For this reason, the Pareto distribution is one of the distributions that is often used to model the tails of another distribution. Generally, if you have a set of observations, and you discard all observations below a threshold, you are left with what are called 'exceedances'. The threshold needs to be reasonably far out in the tail. If from each value of the exceedances you subtract the threshold value, the resulting dataset is estimated by the generalized Pareto distribution.

A mathematical equation with black text Description automatically generated

The Pareto distribution has a 'shape parameter'. The average of two Pareto distributions with tail parameters#1 and#2 (#is a Greek character, pronounced as 'sai' (saa-eee)), is the weighted average of#1 and#2 with weights proportional to the number of observations in the datasets underlying the distributions.

NEW QUESTION # 129

Identify the correct sequence of events as it unfolded in the credit crisis beginning 2007:

I. Mortgage defaults increased

II. Collapse in prices of unrelated assets as banks tried to create liquidity III. Banks refused to lend or transact with each other IV. Asset prices for CDOs collapsed

- A. IV, I, II and III

- B. I, III, IV and II

- C. III, IV, I and II

- D. I, IV, III and II

Answer: D

Explanation:

According to a paper by the BCBS, here is an excellent summary of what happened. Based on this, Choice 'c' is the correct answer.

"At the outset of the crisis, mortgage default shocks played a part in the deterioration of market prices of collateralised debt obligations (CDOs). Simultaneously, these shocks revealed deficiencies in the models used to manage and price these products. The complexity and resulting lack of transparency led to uncertainty about the value of the underlying investment. Market participants then drastically scaled down their activity in the origination and distribution markets and liquidity disappeared. The standstill in the securitisation markets forced banks to warehouse loans that were intended to be sold in the secondary markets. Given a lack of transparency of the ultimate ownership of troubled investments, funding liquidity concerns were triggered within the banking sector as banks refused to provide sufficient funds to each other. This in turn led to the hoarding of liquidity, exacerbating further the funding pressures within the banking sector. The initial difficulties in subprime mortgages also fed through to a broader range of market instruments since the drying up of market and funding liquidity forced market participants to liquidate those positions which they could trade in order to scale back risk. An increase in risk aversion also led to a general flight to quality, an example of which was the high withdrawals by households from money market funds."

NEW QUESTION # 130

Which of the following cannot be used as an internal credit rating model to assess an individual borrower:

- A. Distance to default model

- B. Probit model

- C. Logit model

- D. Altman's Z-score

Answer: A

Explanation:

Altman's Z-score, the Probit and the Logit models can all be used to assess the credit rating of anindividual borrower.There is no such model as the 'distance to default model', and therefore Choice 'a' is the correct answer.

NEW QUESTION # 131

Which of the following methods cannot be used to calculate Liquidity at Risk?

- A. Analytical or parametric approaches

- B. Historical simulation

- C. Scenario analysis

- D. Monte Carlo simulation

Answer: A

Explanation:

Analytical or parametric approaches are not useful at all for liquidity at risk calculations because there are no neat distributions available to parameterize the large number of factors that affect the calculations of liquidity inflows and outflows. Historical simulations, Monte Carlo and scenario analysis (which can complement historical scenarios) are all valid choices

NEW QUESTION # 132

If the duration of a bond yielding 10% is 6 years, the volatility of the underlying interest rates 5% per annum, what is the 10-day VaR at 99% confidence of a bond position comprising just this bond with a value of

$10m? Assume there are 250 days in a year.

- A. 0

- B. 1

- C. 2

- D. 3

Answer: A

NEW QUESTION # 133

Which of the following was not a policy response introduced by Basel 2.5 in response to the globalfinancial crisis:

- A. Stressed VaR (SVaR)

- B. Incremental Risk Charge (IRC)

- C. Comprehensive Capital Analysis and Review (CCAR)

- D. Comprehensive Risk Model (CRM)

Answer: C

Explanation:

The CCAR is a supervisory mechanism adopted by the US Federal Reserve Bank to assess capital adequacy for bank holding companies it supervises. It was not a concept introduced by the international Basel framework.

The other three were indeed rules introduced by Basel 2.5, which was ultimately subsumed into Basel III.

Stressed VaR is just the standard 99%/10 day VaR, calculated with the assumption that relevant market factors are under stress.

The Incremental Risk Charge (IRC) is an estimate of default and migration risk of unsecuritized credit products in the trading book. (Though this may sound like a credit risk term, it relates to market risk - for example, a bond rated A being downgraded to BBB. In the old days, the banking book where loans to customers are held was the primary source of credit risk, but with OTC trading and complex products the trading book also now holds a good deal of credit risk. Both IRC and CRM account for these.) While IRC considers only non-securitized products, the CRM (Comprehensive Risk Model) considers securitized products such as tranches, CDOs, and correlation based instruments.

The IRC, SVaR and CRM complement standard VaR by covering risks that are not included in a standard VaR model. Their results are therefore added to the VaR for capital adequacy determination.

NEW QUESTION # 134

Company A issues bonds with a face value of $100m, sold at issuance at $98. Bank B holds $10m in face of these bonds acquired at a price of $70. What is Bank B's exposure to the debt issued by Company A?

- A. $7m

- B. $10m

- C. $9.8m

- D. $6.86m

Answer: A

Explanation:

Bank B's exposure is measured by the price it paid for the bonds, which in this case is $7m ($10m x 70/100).

Hence Choice 'c' represents the correct answer.

(Note that the question is asking for 'exposure' and not the legal claim in the event of default. The legal claim in the event of default would be the full notional of $10m. ) The initial issue price and issue size are irrelevant.

NEW QUESTION # 135

Which of the following statements is true in relation to collateral management?

I. A collateral management system need not consider the failure by counterparties to returncollateral when due II. The extent to which counterparties may have rehypothecated collateral is not a consideration for a collateral management system III. Cash is an acceptable substitute for any type of collateral required to be posted IV. Haircuts do not apply to treasury issued instruments posted as collateral

- A. I, II and III

- B. II and III

- C. I, II, III and IV

- D. None of the statements is true

Answer: D

Explanation:

Strong management of collateral, both receivable and payable, is emerging as an area requiring significant investment by financial institutions and asset managers in IT infrastructures and business processes. A bank needs to make collateral calls daily, based upon the P&L of the previous day, and likewise receives collateral calls from its counterparties. Just like cash, a bank needs to make sure that it does not run out of collateral to post when a call is received. Interestingly, based upon the agreements between banks and their mutual understanding, only certain types of instruments often qualify as valid collateral - and in such cases even cash is not acceptable if the right type of bond or other agreed security is not available to post. The operational challenges of managing collateral increase manifold due to 'rehypothecation', ie when collateral received from one counterparty gets posted out as collateral where it is due. In such cases, the bank should have the mechanisms to receive the right assets back in a timely way in case rehypothecated assets are to be returned.

The systems should be able to deal with delays, failures without impacting the ability of the bank to post collateral as needed. All of this requires major investments in IT and processes.

Statement I is not true as a bank is bound to post collateral to third parties when needed regardless of the failure of its counterparties to post collateral to it when owed. In the markets, failures by counterparties can and do happen, and a collateral management system needs to account for and keep a buffer for the fact that some collateral when due will not be received.

Statement II is not true as rehypothecation by counterparties of collateral posted increases the chances of the collateral not being received in time. The system should consider the need for liquidity to generate assets that can be posted as collateral when others have failed to return the collateral in a timely way.

Statement III is not correct as cash may not be acceptable to counterparties as collateral. From a practical point of view, they may not have the infrastructure to receive and account for cash as collateral. A Swiss bank, for example, may have an 'account' to receive US t-bills as collateral but may not even have a US dollar account to receive cash. Even if it did, the volumes of transactions going back and forth may make tracking and reconciliations impossible. Thus a bank should always make sure that it has the right type of collateral available to post.

Statement IV is incorrect as well, as treasury issued instruments are also subject to haircuts. Their value also fluctuates in response to changes in yields, and therefore they are subject to haircuts as well.

Thus none of the statements are correct and Choice 'd' is the correct answer.

NEW QUESTION # 136

Which of the following statements are true:

I. Stress testing, if exhaustive, can replace traditional risk management tools such as value-at-risk (VaR) II. Stress tests can be particularly useful in identifying risks with new products III. Stress testing is distinct from a bank's ICAAP carried out periodically IV. Stress testing is a powerful communication tool that can convey risks to decisionmakers in an organization

- A. II and IV

- B. I, II and III

- C. I and III

- D. All of the above

Answer: A

Explanation:

Stress testing provides an independent and complementary perspective to other risk management tools such as value-at-risk and economic capital. Both are tools that serve similar purposes but are not interchangeable.

Stress testing, no matter how exhaustively done, can not replace other tools such as those based on analytical or historical models. It can provide a useful sense check to validate models and assumptions, but is not a replacement for traditional techniques. Therefore statement I is false.

Stress testing can certainly help identify risks with new products for which historical data may be limited, and analytical models may be based upon many unproven assumptions. It can help challenge the risk characteristics of new products where stress situations have not been observed in the past. Therefore statement II is correct.

ICAAP stands for the 'internal capital adequacy assessment process' performed by a bank (remember the acronym and its expansion). Stress testing is an integral part of a firm's ICAAP, and not distinct. It is one of the elements of the internal process. Therefore statement III is false.

Statement IV is correct as stress testing is indeed a powerful tool that can communicate risks throughout the organization as the stress scenarios are easier to comprehend than arcane statistical models. They are also easier to explain to regulators, and are a powerful communication tool.

Thus Choice 'c' is the correct answer.

NEW QUESTION # 137

A risk management function is best organized as:

- A. integrated with the risk taking functions as risk management should be a pervasive activity carried out at all levels of the organization.

- B. reporting directly to the traders, as to be closest to the point at which risks are being taken

- C. a part of the trading desks and other risk taking teams

- D. report independently of the risk taking functions

Answer: D

Explanation:

The point that this question is trying to emphasize is the independence of the risk management function. The risk function should be segregated from the risk taking functions as to maintain independence and objectivity.

Choice 'd', Choice 'c' and Choice 'a' run contrary to this requirement of independence, and are therefore not correct. The risk function should report directly to senior levels, for example directly to the audit committee, and not be a part of the risk taking functions.

NEW QUESTION # 138

Which of the following belong to the family of generalized extreme value distributions:

I. Frechet

II. Gumbel

III. Weibull

IV. Exponential

- A. II and III

- B. IV

- C. I, II and III

- D. All of the above

Answer: C

Explanation:

Extreme value theory focuses on the extreme and rare events, and in the case of VaR calculations, it is focused on the right tail of the loss distribution. In very simple and non-technical terms, EVT says the following:

1. Pull a number of large iid random samples from the population,

2. For each sample, find the maximum,

3. Then the distribution of these maximum values will follow a Generalized Extreme Value distribution.

(In some ways, it is parallel to the central limit theorem which says that the the mean of a large number of random samples pulled from any population follows a normal distribution, regardless of the distribution of the underlying population.) Generalized Extreme Value (GEV) distributions have three parameters: # (shape parameter), # (location parameter) and # (scale parameter). Based upon the value of #, a GEV distribution may either be a Frechet, Weibull or a Gumbel. These are the only three types of extreme value distributions.

NEW QUESTION # 139

When pricing credit risk for an exposure, which of the following is a better measure than the others:

- A. Notional amount

- B. Mark-to-market

- C. Potential Future Exposure (PFE)

- D. Expected Exposure (EE)

Answer: D

Explanation:

Exposure for derivative instruments can vary significantly over the lifetime of the instrument, depending upon how the market moves. The potential future exposure represents the extremes, notthe most likely outcome.

The expected exposure is the most suitable measure for pricing the credit risk. Over time, as multiple transactions are entered into, the expectation (or the mean) will be realized - though individual transactions may have more or less by way of exposure.

The notional amount may not be relevant, though for loans it may be the most important contributor to the expected exposure. Mark-to-market will represent the exposure at a given point in time, but cannot be predicted nor be used to price the credit risk.

NEW QUESTION # 140

The loss severity distribution for operational risk loss events is generally modeled by which of the following distributions:

I. the lognormal distribution

II. The gamma density function

III. Generalized hyperbolic distributions

IV. Lognormal mixtures

- A. I, II and III

- B. II and III

- C. I and III

- D. I, II, III and IV

Answer: D

Explanation:

All of the distributions referred to in the question can be used to model the loss severity distribution for op risk. Therefore Choice 'c' is the correct answer.

NEW QUESTION # 141

Under the credit migration approach to assessing portfolio credit risk, which of the following are needed to generate a distribution of future portfolio values?

- A. All of the above

- B. The forward yield curve

- C. A specified risk horizon

- D. A rating migration matrix

Answer: A

Explanation:

The credit migration approach to assessing portfolio credit risk involves obtaining a distribution of future portfolio values from the ratings migration matrix. First, the frequencies in the matrix are used as probabilities, and expected future values of the securities belonging to each rating category are calculated.

These are then discounted to the present using the discount rate appropriate to the 'future' rating category. This gives us a forward distribution of the value of each security in the portfolio. These are then combined using the default correlations between the issuers. The default correlation between the issuers is often proxied using asset returns, and recognizing that default occurs when asset values fall below a certain threshold. A distribution for the future value of the portfolio is generated using simulation, and from this distribution the Credit VaR can be calculated.

Thus, we need the migration matrix, the risk horizon from which the present values need to be calculated, and the forward yield curve or the discount curve for each rating category for the risk horizon. Thus, Choice 'd' is the correct answer.

NEW QUESTION # 142

......

Download Free Latest Exam 8011 Certified Sample Questions: https://pass4sure.actualtorrent.com/8011-exam-guide-torrent.html